Marriott, the Income Specialists, contemplates the investment landscape in a post-QE world

Since 2008 the investment landscape has largely been shaped by quantitative easing (QE) – the process of creating money to buy bonds. This form of monetary policy, which is designed to stimulate economic growth, has served the secondary purpose of aiding the performance of certain financial markets. For instance, first world bond yields declined substantially through this period. As a result of these low yields foreign money flowed into emerging markets in search of higher yields.

The US Federal Reserve Bank is anticipated to bring this uncommon form of monetary stimulus to an end in 2014. Although the winding down process will be gradual, the investment implications are profound. The underperformance of emerging markets relative to first world markets is likely to continue while it is also highly probable that the 10-year bull market in South African bonds and listed property ended in 2013. Inflationary pressures and rising interest rates will add upward pressure to bond and property yields.

2013 was a challenging year for South Africa

In 2013, investors saw a glimpse of what the investment world might look like without QE. The prospect of tapering in the US created a high degree of currency and market volatility, particularly in emerging markets.

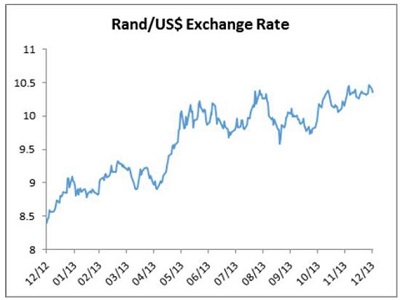

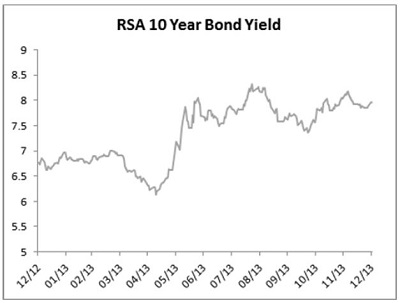

South Africa was one of the economies most impacted by this, due to our reliance on foreign capital to fund our large fiscal and current account deficits. The volatility of the rand against the US dollar and the volatility of the 10-year RSA bond yield during 2013 can be seen in Charts 1 and 2.

Chart 1: US$/Rand Exchange Rate (31 December 2012 to 31 December 2013)

Chart 2: 10-Year Bond Yield (31 December 2012 to 31 December 2013)

First world markets comfortably outperformed emerging markets in 2013, in both rand and dollar terms (see Table 1).

Table 1: Total return in rand and dollar terms from selected first world and emerging markets

The significant divergence in performance may be attributed to the deteriorating economic conditions of emerging markets relative to first world economies and the more attractive dividend yields on offer in these regions.

At Marriott Asset Management, we have long recognised that QE would not continue indefinitely and, consequently, our portfolios were structured in preparation for the market events of 2013.

1. Investors’ offshore exposure has been maximised to the better-performing first world equity markets.

2. Fixed interest bonds and property have been avoided. The recent hike in short term interest rates is indicative of a rising trend in inflation and interest rates. This will put upward pressure on property and bond yields, resulting in a decline in capital value.

3. Domestically, only companies that will be resilient to a challenging economic environment are held in our portfolios.

2014 heralds a world without Quantitative Easing

“South Africa may be more exposed than other emerging markets to capital flow reversals because of its relative high current account deficit, risky funding mix, high share of non-resident holdings of government debt and liquid financial markets.” IMF Country Report, 2013

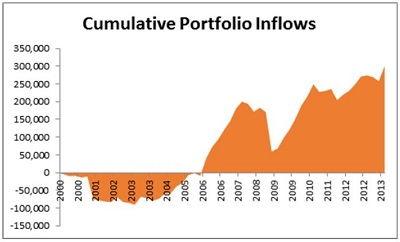

In December 2013, after months of speculation, the US Federal Reserve Bank announced it would officially begin reducing its QE programme. This is likely to mean continued rising US bond yields and, as a result, less foreign flows into South Africa. Chart 3 below highlights the cumulative value of foreign portfolio inflows into the South African market since 2000.

Chart 3: Cumulative Value of Foreign Portfolio Inflows into SA

This abundance of foreign capital has, to a large extent, kept South African government bond yields low, the rand strong and has allowed the country to live beyond its means for a number of years. With a high probability of foreign capital being less accessible in the years ahead, our expectations are for continued rand volatility, higher inflation and rising bond and property yields.

Given this scenario, the implications for the different asset classes can be summarised as follows:

• SA Cash: The rand has lost approximately 55% of its value against the US dollar over the last three years. Although subdued domestic demand has helped contain the inflationary impact of this depreciation, it is likely going forward that companies will be forced to pass on higher costs to consumers. This could well prompt the SA Reserve Bank to continue raising interest rates in 2014.

• SA Bonds: The South African fixed interest bond market is likely to come under increasing pressure as a result of the reduction of QE in the US and the potential for higher inflation and rising cash interest rates domestically. Inflation-linked bonds have better prospects due to guaranteed inflation protection.

• SA Listed Property: Due to the high correlation between bond and property yields and the continued upward pressure on bond yields, South African listed property is likely to perform poorly in 2014.

• SA Listed Equities: In a subdued economic environment, it is difficult to justify the current low dividend yields of local equities. As a result of below-average yields, the impact of dividend growth on investment value growth will be even more important in the years ahead. Companies which are able to grow their dividends consistently are likely to serve investors best.

• International Listed Real Estate Investment Trusts: International real estate continues to offer investors fair yields with inflation-hedged income growth prospects.

• Direct UK Real Estate: Direct A grade real estate in the UK is offering investors exceptional yields.

• International Fixed Interest Bonds: Despite a substantial increase in the yields of US, UK and Euro-Zone 10-year fixed interest bonds, yields remain below historic averages presenting investors with capital risk.

• International Equities: Based on current valuations it is possible to invest in some of the largest and most recognisable companies in the world on acceptable dividend yields with solid dividend growth prospects. This asset class is currently offering investors best value.

With similar risks likely to prevail in 2014, investors should maintain much of last year’s investment strategy

It is clear that as quantitative easing is scaled back, the yields of bonds and local listed property are likely to continue to rise. These asset classes will continue to present capital risk until such time as yields have fully adjusted to an investment world without central banks printing money. With regards to local equity exposure, investors will be best served with a portfolio of companies with the ability to grow their dividends regardless of economic circumstances.

The opportunity for investors remains in first world markets where large capitalisation multinationals are trading on high dividend yields. With economic growth prospects steadily improving in these regions and taking into consideration the Rand’s vulnerability to a slowdown in foreign capital inflows, the investment case for offshore equities remains compelling.

This release has been issued on behalf of Marriott Asset Management

For more information contact:

Marriott Asset Management:

Bronwen Barclay, Head of Marketing & Distribution:

031 765 0736 or 083 797 9979

Shirley Williams Communications

Shirley Williams 031 564 7700 or 083 303 1663

Gillian Findlay 082 330 1477

About Marriott Asset Management

The Income Specialists aim to reduce financial anxiety of retired investors by offering Solutions for Retirement, using an Income Focused Investment Style which produces reliable and consistent monthly income.

© 2005 - 2026 | Portfolio Property Investments | Powered by the PPI Business Platform