International Property – Global Residential Market Forecast 2011

GLOBAL VIEW

In this first edition of our global residential market forecast, Liam Bailey, Knight Frank’s Head of Residential Research, considers why house prices are now rising in the majority of countries across the world.

It has been a remarkable period for global housing markets. Prices have boomed, crashed and, in some markets, boomed again – all in the space of five years. To understand the reasons for the latest upturn in this rollercoaster ride we need to step back and briefly examine the reaction to the recent crash.

The first signs of the global downturn were seen in Israel in early 2006, when prices began to slip on the back of tightening credit availability. The real catalyst for the fall, however, was the reaction of banks to the emerging sub-prime crisis in the US. Prices there began to fall as early as summer 2006.

From that point forward, prices peaked and started an inexorable slide across the world. The whole process took two years to play out, hitting Portugal and Ireland in late 2006, moving through the UK, Latvia, New Zealand, Denmark and Hungary during 2007 and finally afflicting Croatia, The Czech Republic, Finland, France, Greece, Hong Kong, Iceland, Singapore and China in 2008.

On average, prices fell by around 17% across the globe during 2007 and 2008. The next logical phase of the market cycle, bearing in mind the problems gripping most developed economies at the time, would have been for prices to languish at these low levels. Instead, much to the surprise of many, they began to bounce back.

Since early 2009, global house prices have recovered, on average, by 10%. By mid 2010, values were only around 9% below their 2006-2008 peak. After a decade and a half of rising prices, which had seen growth of 100%, 200%, or even 300% in some markets, a 9% decline doesn’t actually seem like a catastrophe.

Despite recent growth, there are several countries where prices are still well below the peak of the market. The US, down 31%,is the most high profile, but a range of European countries, which were the worst casualties of the speculative investor bubble that formed in the run up to the credit crunch, are still suffering badly. Values in Lithuania, for example, have dropped by an incredible 63%. Latvia (-43%), Bulgaria (-34%) and Ireland (-31%) have also fared very badly.

Unintended consequences

In most countries the recent upturn in prices can be explained by the unintended consequences of the economic stimulus measures put in place by governments. Ultra-low interest rates and targeted support for the banks have encouraged house buyers, especially the affluent, to enter the market. This increase in demand has helped push prices higher.

So how has the latest recovery phase been experienced across the globe? Arguably, the most noticeable trend in global house prices is the ease with which the performance of global housing markets can now be grouped by world region. The top positions in our rankings are all occupied by Asia-Pacific locations, while, despite recent growth, Europe still dominates the bottom half of the table.

The most obvious sign of the recovery in the global housing market is that 61% of countries recorded positive growth in the 12 months to mid 2010. This is some way off the figure of 90% recorded in early 2006, but significantly higher than the 35% seen in the 12 months to mid 2009.

Data from the second quarter of 2010 suggests that the recovery is continuing to spread. Analysis of our quarterly growth results suggests that the markets in some of the worst-performing locations, such as the Baltic States and Ukraine, are beginning to experience some respite, with prices falling at a slower rate than previously. Prices in Estonia, for example, fell by 40% in the 12 months to June 2010, but actually rose by 0.4% rise during the second three months of the year.

In Asia, prices continue to rise, despite strenuous efforts from governments to control and limit growth. The Chinese market has performed spectacularly over recent years, but there is growing evidence here of a rapid slowing in price growth following concerted government action to avoid a bubble and bust scenario.

Turning our focus beyond recent and current pricing trends, over the next few pages we consider the outlook for the global housing market, in terms of risks, pricing and market stability.

MARKET RISKS

The global residential market is undoubtedly in a stronger place than it was in mid-2008 or 2009, but as we move through the second half of 2010 the number of risks to the sector seem to be rising.

Knight Frank’s global research team has just conducted a detailed risk assessment of the threats facing the world’s property markets.

In figure 3 we have set out our headline results, with a ranking of each broad risk category from 0 to 10, where 0 represents ‘no risk’, 5 ‘moderate risk’ and 10 ‘significant risk’.

We uncovered a noticeable degree of regional variation between the views from our contributors, and to reflect this we have split our results by ‘Asia’ and ‘Europe and US’ responses.

The most notable trend from our assessment, was that the Asian respondents to our survey were more bearish than those in Europe or our US respondents across all categories, with the exception of the risk from rising inflation.

The leading factor for the more negative stance from Asia was a concern regarding the position of the region’s markets in the property market cycle. While prices have fallen, sometimes significantly, in the West over the past few years, in the majority of Asian markets prices either fell only marginally from 2006 or 2007, or indeed didn’t slip at all. In almost all cases the leading Asian housing markets are substantially higher than the levels seen before the credit crisis first infected the global economy. In short, industry experts in Asia seem to feel that the continent cannot escape weakening market conditions.

Considering the results in detail, the fear of a double dip recession is high on the list – the very strong relationship between GDP growth and house price performance points to the risk posed by a global economic slowdown.

However, the biggest single theme to emerge from our assessment is the significance ascribed to debt problems – both private and public, an issue we return to on page four of this report.

The potential of these existing debt problems to feed into lower new lending volumes, is also noted in our results. In Asia mortgage market risks are aggravated by recent and future plans for government-imposed borrowing restrictions.

For example, additional credit controls imposed in China are reducing capital flows into Hong Kong, which is acting to slow the market there.

Fears over the impact of inflation or alternatively deflation were not thought to be significant issues for the market – suggesting that at least for the second half of 2010 and for 2011, the rising cost of mortgage finance ought not to be a critical factor for the market. Although in one market at least, Russia, the cost of mortgage finance is becoming more problematic.

Interest rates for mortgage loans in Russia are very high compared to most European markets, with rates of between 11% and 17% not being uncommon. For some buyers it has become more common to rely on alternative sources of finance other than bank loans, with investors looking to sell part of their portfolios to raise the required equity for purchases.

Political risk was thought to be of minimal importance to our European and US contributors, however, the potential for this topic to become more significant is something we consider later in this report.

Cross-border trading

One of the main drivers of price and demand growth in residential markets in the more ‘international’ markets – for example, Europe including London and the main southern European sun-belt markets; the US covering Florida and New York; but also the main Asian and South American second home markets – has been the expansion of cross-border purchasing activity.

As an example of the importance of this market, in the 12 months to June this year 50% of all new build apartments in central London were bought by foreign nationals.

As the world economy has grown, so the restrictions around capital transfer have declined. In more and more locations it has become easier to take equity from one country to another.

In figure 4 we can see that the rules around capital transfer are expected to be further relaxed over time. Ironically, in figure 5 we can see that there is a perceived risk, especially from the Asian contributors, that the ongoing expansion of crossborder trading should not be regarded as a given. While in most markets there is a desire to see an expansion of inward investment, this is not always the case, parts of Switzerland being a prime example. In others, the political or security situation is such that foreign investment has fallen away and therefore so too has a key support for the market.

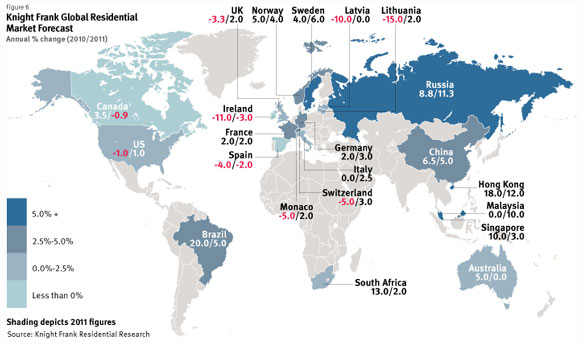

2011 MARKET FORECAST

The post-crash bounce in global housing markets is set to slow considerably in 2011. However, lower price growth across the world masks improving fortunes in Europe and a more sustainable rate of market performance in Asia.

The countries that were worst effected by the residential market downturn, Spain, Ireland and a clutch of Eastern European locations, did not experienced any respite during 2009 or early 2010 – in fact prices in some parts of Ireland are now lower by almost 50% from their late-2006 peak.

These markets are set to experience further price falls over the next 18 months, although the rate of decline will slow, with -11% expected in Ireland in 2010 compared with only -3% in 2011. Some of the most troubled markets in Eastern Europe, Latvia and Lithuania for example, are expected to post positive growth next year for the first time in three years.

The key driver in these locations is that prices are actually beginning to return to something close to a “sustainable” level. This is partly because the relationship between prices, rents and incomes is falling more in line with their long-run average.

In locations like the UK, France, Australia and Canada, prices have performed well over the past 18 months. In the UK and France this has happened on the back of low rates and stimulus measures. In Australia a burgeoning economy tied into Asia’s economic boom has been the driver. However, these are all examples of markets that stand well above long-term measures of ‘fair pricing’.

In the UK we expect that the second half of 2010 will see prices fall following the introduction of austerity measures by the government, such as tax hikes and spending cuts, but most importantly due to a shrinking mortgage market. However, a modest annual fall of 3.3% will not address the risk of a more significant adjustment should interest rates rise strongly from 2011 onwards.

While the US appears to be experiencing a second wave of difficulties in terms of defaults and distressed loans, and again turnover volumes are at historically very low levels, it looks reasonable to assume that pricing will probably remain relatively static over the next 18 months. The US is one market that has actually seen pricing return to much more realistic and sustainable levels over the past three years.

Turning to Asia, we can see the real driver behind our global view of price moderation in 2011. We expect a significant slowing in the rate of growth in locations like Hong Kong (18% in 2010, down to 12% in 2011), Singapore (10% to 3%), Australia (5% to 0%) and China (7% to 5%).

As we discuss on page 4 – the risks to the above forecast are significant – however our central scenario is that the global housing market will deliver positive growth in 2011 overall.

TRENDS TO WATCH IN 2011

The withdrawal of market support

The more blatant forms of government support for the housing market, including first time buyer concessions in the UK and Australia, and tax incentives in the US, either have, or are in the process of being, withdrawn. Most noticeably in the US this has certainly led to a slower housing market, with falling sales volumes. The real test for market resilience, especially in Europe and the US, is likely to come at some point in 2011 when interest rates begin to climb from their current historic lows. On our measures the UK is one of the markets most at risk from this process.

Continuing weak new-build supply in the West

The market crash brought the construction sector to a virtual halt across much of Europe and the US. By 2009 there was the beginning of a sharp improvement in volumes, in Europe particularly, which largely continued through the first half of 2010. Funding constraints, for both developers and purchasers, will begin to limit the recovery in development volumes in 2011, meaning that a structural undersupply of housing will contribute to slightly higher than trend rates of price growth from 2012 and beyond. There will be some noticeable exceptions to this trend, due to a continuing and significant over-hang of supply, the US, Spain, Ireland being the prime examples.

Government activism

The confidence with which governments across the globe are looking to influence, if not control, their national housing markets is undimmed. In Hong Kong, for example, there is a sense that the government’s efforts to rein in an overheated market are beginning to take effect. These include measures to increase land supply and a maximum 60% loan-to-value restriction on mortgages for luxury homes. Developers are now also required to release at least 30% of units in the first phase of their projects to halt the slow release of homes that has allowed prices to inflate over the course of the development. This new wave of government activism is not limited to Asia and we expect to see more mortgage market controls in Europe and potentially north and south America in 2011.

The debt drag

The most significant factor which will determine the performance of the global housing market in 2011 will be the ability of lenders to continue to offer new funding to the market in an environment where debt levels are still critically high in the West. In Asia and most emerging markets, with lower consumer debt, the issue is far less acute, and mortgage market debt is still a fraction of western levels. But in Europe and the US, existing indebtedness and the lack of funding opportunities for lenders will begin to see limits on mortgage lending and we should not be surprised to see the extension of mortgage rationing.

Courtesy: Knight Frank Residential Research

© Knight Frank LLP 2010

This report is published for general information only and not to be relied upon in any way. Although high standards have been used in the preparation of the information, analysis, views and projections presented in this report, no responsibility or liability whatsoever can be accepted by Knight Frank LLP for any loss or damage resultant from any use of, reliance on or reference to the contents of this document. As a general report, this material does not necessarily represent the view of Knight Frank LLP in relation to particular properties or projects. Reproduction of this report in whole or in part is not allowed without prior written approval of Knight Frank to the form and content within which it appears.

For further information, please contact:

Liam Bailey, head of residential research, Knight Frank,

T +44 20 7861 5133

M +44 7919 303148

Andrew Shirley, head of rural property research, Knight Frank,

T +44 20 7861 5040

M +44 7500 816217

James Kennard, research consultancy, Knight Frank,

T +44 20 7861 5134

M +44 7500 065142